Navigating the Future of Social Security and Medicare: What You Need to Know Now

What’s Really Happening with Social Security and Medicare?

According to the 2025 Social Security Trustees Report, the Old-Age and Survivors Insurance (OASI) Trust Fund and the Disability Insurance (DI) Trust Fund combined can pay 100% of scheduled benefits until about 2034.

The OASI Trust Fund—the primary source for retired worker and survivor benefits—can pay full scheduled benefits until 2033. After that, without legislative action, beneficiaries would receive about 77% of scheduled benefits solely from incoming payroll taxes.

The DI Trust Fund is expected to cover 100% of total scheduled benefits through at least 2099, which is the final year of the 2025 Trustees Report’s projection period.

If the two funds were combined, the hypothetical OASDI reserves would be depleted in 2034, at which point 81% of scheduled benefits could still be paid. However, combining these funds would require a change in the law. If Congress acted to merge them, it would trigger an automatic 19% benefit cut or force higher payroll taxes to maintain solvency.

Medicare’s Hospital Insurance (HI) Trust Fund, which finances Part A, is expected to pay full benefits until 2033. Beyond that, program income would cover 89% of scheduled benefits. By contrast, Part B and Part D, financed through the Supplementary Medical Insurance (SMI) Trust Fund, are considered adequately funded indefinitely due to annual funding adjustments. History and politics suggest that drastic benefit cuts for current or near retirees are unlikely. Social Security and Medicare have long been considered the political “third rail,” too politically charged and controversial to cut—which makes it probable Congress will act to avoid steep cuts for those already receiving or close to receiving benefits.

What Funding Solutions Are on the Table?

Congress has many options to bring Social Security back to long-term financial health—most with minimal impact on current or near retirees if acted on soon. Some of the discussed solutions include:

- Gradual payroll tax increases. For example, increasing the current 6.2% employee and employer payroll tax rate would address the 2034 gap, especially if phased in gradually rather than enacted in a single year.

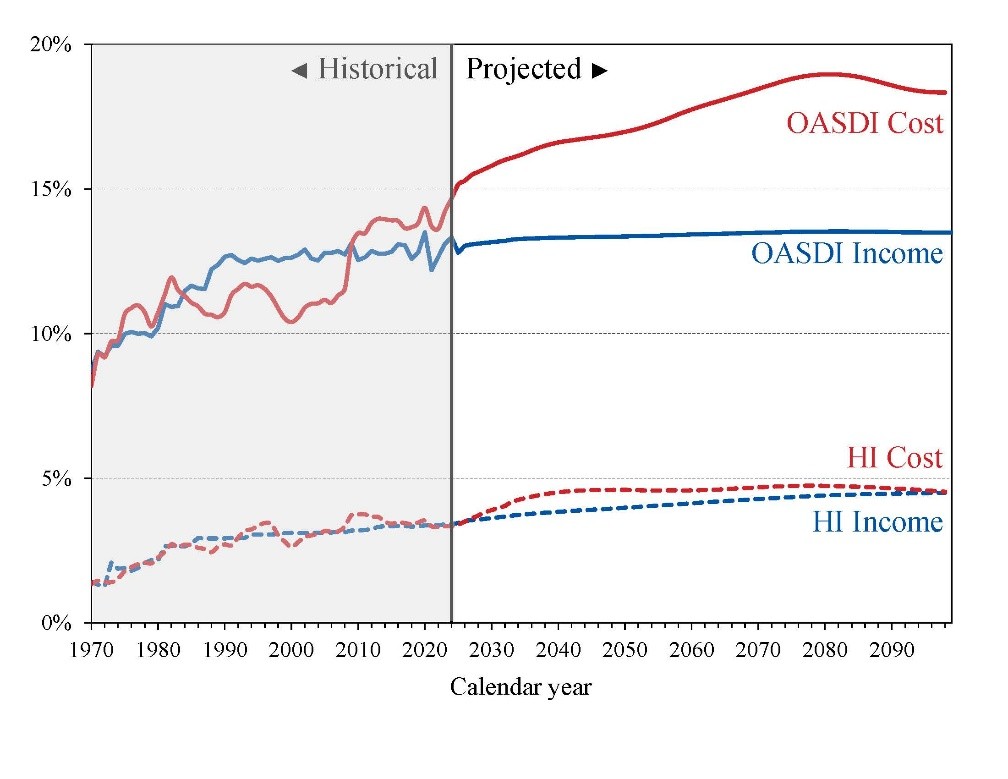

Eliminating or raising the taxable earnings cap on Social Security. Currently, only wages up to $176,100 (as of 2025) are subject to Social Security taxes. There is no maximum cap on Medicare, which results in a much tighter gap as represented in the chart below. Removing or increasing this cap could close much of the shortfall.

Chart A—OASDI and HI Income and Cost as Percentages of Their Respective Taxable Payrolls

- Raising the retirement age. Given increased life expectancies, gradually moving up the full retirement age for younger workers could help. Importantly, any changes would likely be phased in to avoid sudden shocks.

- Other methods, including making a larger portion (possibly up to 100%) of Social Security benefits taxable, capping cost-of-living adjustments (COLA), or using general revenue funds, are also being considered.

None of these solutions, by themselves, are likely to impose sudden major cuts on those already retired or close to retiring. Phased-in changes give people time to plan and adjust.

Should I Claim My Benefits Early?

Many people worry and consider starting Social Security benefits at 62 rather than waiting until full retirement age or until 70. While the concern is understandable, starting early typically results in about a 30% permanent reduction in your monthly benefit compared to waiting until 70.

Don’t let fear dictate your claiming decision. Waiting until age 70 remains the best financial choice for most healthy individuals and acts as a valuable “insurance policy” against the risk of outliving your assets.

Factor longevity into your plan. Consider using online tools to estimate your life expectancy based on health and family history. For those with substantial assets, Social Security functions much like an annuity, and delaying benefits increases the guaranteed income stream providing security.

Expect change, but not chaos. Some adjustments will be necessary, but drastic cuts for those near or in retirement remain unlikely. The most important strategy is staying informed and flexible.

What Steps Can I Take Now to Protect Myself?

Set up your official Social Security website account. By registering, you prevent scammers from creating fake profiles and potentially claiming your benefits before you do. This is important even for younger clients far from retirement, as it also allows you to monitor your recorded work history. Social Security statements are mailed periodically (though the frequency may vary) and provide a snapshot of your earnings and projected benefits.

The Bottom Line

Social Security is facing real challenges, but numerous practical policy solutions exist. For most clients, the best approach is to make a personal benefits plan based on your own health, longevity, and financial needs—not on headlines or political noise. We’ll keep you updated as changes evolve and are here to help answer your Social Security questions.

Sources

https://www.ssa.gov/oact/trsum/