WESCAP Q2 Quarterly Commentary: Investor Sentiment, Cooling Inflation, and Artificial Intelligence

Portfolio results for the second quarter of 2023 were generally positive for stocks and negative for long-term bonds. For the quarter, the S&P 500, EAFE index (foreign stocks), and long-term Treasury bonds (Bloomberg/Barclays 20+ Yrs) returned +8.7%, +3.0%, and -2.4%, respectively.

The debt ceiling impasse was successfully concluded. As a result, June saw a large rally in most global stock indices. Investor sentiment turned positive as shown by the bullish late June AAII weekly investor survey and with S&P 500 volatility sharply dropping.

Adding to investor confidence was economic data showing a strong-enough economy and a resilient labor market despite the Federal Reserve’s restrictive monetary policy. Inflation continues to cool off as supply chain issues and oil/energy shortages have largely receded.

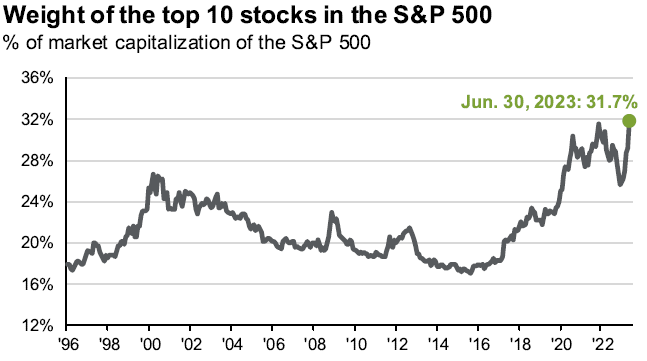

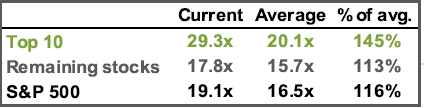

Growing enthusiasm regarding the prospects of Artificial Intelligence (AI) has boosted the valuations of the 10 largest firms in the S&P 500 to unprecedented levels. The lower left graph (J.P Morgan, Q2 Guide to the Markets) shows that the 10 largest firms within the S&P 500 now account for 31.7% of the value of the entire index. This is higher than the nearly 27% index valuation of the largest 10 stocks at the height of the internet bubble in early 2000. The lower right table shows that the current price/earnings (P/E) ratio of the largest 10 stocks is at a 45% premium to their average P/E ratios from 1996 to the present.

It is possible that AI will be even more transformative than the internet. However, stock prices can get ahead of actual progress. This happened with the internet bubble that burst in 2000, which resulted in about a 12-year period in which the S&P 500 failed to make a positive return for an investor that owned it at its 2000 peak, a long time not to make money. Current extreme market and earnings valuations of the 10 largest stocks in the S&P 500 are very similar to the peak of the dot-com bubble in 2000. Owning the other 490 stocks in the S&P 500, plus owning mid-cap, small-cap, and many more reasonably valued foreign stocks is likely to be a superior formula for favorable stock returns over the next 5 or more years.

Also, there is nothing wrong with owning T-bills with 5%+ yields, the highest in over a decade. Other fixed-income assets also may generate higher than S&P 500 returns over the next 5 years.

As always, please feel free to contact your WESCAP advisor if you would like to discuss any of this further.